Too Big to Pop

The everything bubble didn't burst. It collapsed into an economic black hole.

At seventeen I worked full time at In-N-Out for about 9 months between my early graduation and college. At the time, In-N-Out treated its people well enough that the line was a career, staffed by people ten, twenty, thirty years older than me. They weren’t failing at anything. They showed up, worked incredibly hard, passed the paycheck-to-paycheck audit every two weeks without missing and… most of them were never going to own a home. Not because of any decision they’d made. The economy changed while they weren’t looking, and everybody on the line knew it without anyone saying it.

Years later I run a finance firm and the feeling from that kitchen hasn’t gone away. Now I at least understand the mechanics to explain it.

Here’s an honest inventory of my own position in this economy. I don’t know my mailman. I don’t know my landlord. I don’t have much hope of ever owning in the neighborhood I live in (and the ticket to hope was building a firm). I park my savings at a bank that lends it to people I don’t know to make money for people I don’t know, and I invest the rest in index funds full of companies I don’t like and, as a customer, often feel abused by. For years I worked a job that didn’t fulfill me, just to pay rent on a drafty building somebody’s parents put up seventy years ago.

It’s no complaint - I’m doing fine, better than most. But it is an observation about structure: nobody in that loop knows me, and I don’t know them. The economy plugs away solving our problems, and requiring us to solve others, without any real sense of accountability other than not running out of cash.

That’s the dissonance of the moment. The scoreboard; stock market, jobs figures, even cash in our savings; says things are fine while our gut says the game is rigged, and I’d argue that the gut is doing the real analysis. It has picked up on something specific: the mechanism that’s supposed to hold everyone in this economy accountable has developed a dead zone at the top.

I call it the Economic Black Hole. To see it we have to start with what money actually is.

The Audit

Cash is an intermediate for trust. It gets created by borrowing (the federal government borrows from the Fed, a business borrows from a bank, you borrow from your uncle) and every one of those loans is a trust judgment with a price attached to it. Interest is the price of doubt (or risk of non-repayment), while inflation is trust growing faster than the problems it's supposed to be solving.

Assets are a different, more real, animal. An asset is the systems, people, and processes, plus the buildings and machines and raw inputs, that directly solve a problem somebody has. “Financial Assets” such as a stock certificate, a deed, an LLC interest are claims on that machinery, not the machinery itself.

Now for the part of capitalism’s grand vision that I’ve actually come to admire. Everyone needs cash to survive and pay rent, groceries, payroll, or debt service. So, every participant in the economy, on a roughly monthly cycle, is forced to sell something (labor, product, inventory, time) at a price someone else sets. That’s the audit. You submit your contribution to the market, the market tells you what it’s worth, and you don’t get to argue, because you have to eat.

The audit comes in three forms:

Consumption is the one nobody at the bottom escapes: you have to sell to eat, and the market prices you monthly whether you like the verdict or not.

Investment is the audit you volunteer for: when you convert surplus into assets you’re submitting a judgment about which problems are real, and your returns are the grade.

Taxation is the public audit, and I’ll say the unfashionable thing and defend it. Cash is trust, sure, but trust denominated in what? In a unit the public maintains. Courts that make a deed enforceable, registries, roads the trucks actually run on, the currency itself. If you accumulate trust in the public’s unit, the public gets to audit the pile on a schedule. That isn’t the state skimming your output so much as the upkeep on the machinery that makes your money mean anything to a stranger. And it happens to be the one audit designed to reach piles the market can no longer touch. Nobody has to enjoy it. Audits keep trust honest, that’s all they’re for.

This audit is the exact reason my firm exists in the form it does. I didn’t have the ability to build the exact thing I wanted on my vision board. It was built this way because we all need cashflow to survive, and the fastest honest route to cashflow was becoming genuinely useful to founders who needed a real financial counterpart. The audit disciplined me into contribution quickly, which is why I still sell my time for money.

The people on that In-N-Out line were passing the same audit I was, every two weeks, without fail. And the system’s implied promise was never “work forever.” It was work, run a surplus on your production of value, convert the surplus into assets, and eventually the assets pass the audit for you. That was the deal.

What broke is symmetrical and opposite at each end: the audit has been made permanent at the bottom and cancelled at the top.

At the bottom, the assets you’re supposed to graduate into (a house, to name the most obvious one, given the scale of cash outflow) have outrun wages so badly that the surplus may never be converted. The audit just repeats, monthly, forever, for people who are contributing the entire time. A wage earner is the most thoroughly audited part of the entire economy, priced by the market every month and taxed by withholding before the paycheck even lands.

At the top, three mechanisms now let accumulated trust skip the audit entirely. Before I name them, a confession.

The Confession

I funded this firm with a margin loan against a portfolio I built during my years in private equity. Most of my startup capex was time, so I worked night shifts on the early build while the loan carried the initial runway when I went full-time. Mechanically that’s the same move as the most notorious wealth strategy in America: borrow against your assets instead of selling them.

So, I’m not going to tell you this mechanism is the sin. Here’s the actual difference. My loan didn’t exempt me from the audit; it merely delayed it while committing me to march further into it. If I didn’t build something clients would pay for, the position would unwind and the market would hand me its verdict.

On the flip side, as the business grew, I didn't rush to pay the loan down. Instead investing the new cash into more assets, which lowers the borrowing burden without lowering the balance, and gave the bank more collateral and less risk. Structurally that's the same move as buy, borrow, die. The only difference is altitude. My assets aren’t appreciating faster than my life could ever need, so the audit is still there waiting for me at the bottom of the loan. Theirs isn't waiting at all.

Ultimately, below a certain altitude, borrowing against your assets is a bridge back into the audit while above a certain altitude it’s escape velocity. That altitude has a mathematical definition: it’s the point where your assets appreciate faster than your interest plus your cost of living. Past that line the forced sale never comes. Not this year, not in your lifetime, and (we’ll get there) not even at your death.

Below the line you sell to live. Above it, you never have to sell anything at all.

The Three Escape Hatches

1. Never sell

Buy, borrow, die. The largest holders of the most-loved assets don’t sell them. They borrow against them at bank-grade spreads, live and reinvest off the proceeds, and when they die the cost basis steps up and the estate repays the loan without the gain ever being taxed. One structure, and it cancels two audits at once: no forced sale, so the market never renders a verdict, and no realization, so the public audit never comes due.

It’s worth being precise about the mechanics: First, every one of those borrowed dollars is a new deposit created against an asset that never traded. Fresh cash minted against unsold trust. Second, removing the sell pressure of the very largest holders turns asset prices into a ratchet. The first-order effect isn’t the price of eggs, though it leaks in eventually. It’s that the assets everyone below the line is trying to graduate into, a house or a share of the future, only get more expensive relative to the wages that are supposed to buy them.

Alongside this the estate tax quietly along the way: the estate tax was a terminal public audit, the one margin call nobody used to escape, and stepped-up basis cancelled the lifetime of capital gains that came with it alongside a now $30MM hurdle before estate taxes start to kick in for couples.

2. The Intake Fan.

Every month, retirement contributions flow into index funds that buy the biggest holdings automatically. No judgment of contribution, no doubt priced in, just size buying more size. I don’t blame anyone for this, indexing is how normal people escaped paying two-and-twenty for underperformance, and every individual in the chain is behaving rationally inside broken plumbing.

But step back and it’s the investment audit automated out of existence, flows that grade no one’s paper. The aggregate physics are wild too. Research on the Inelastic Markets Hypothesis (Gabaix and Koijen) suggests that inflows into the market create large and permanent price increases. Price stops being a verdict on value creation and instead becomes evidence for more price. The scoreboard feeds itself, and when the market wobbles the state steps in, because the biggest collateral pools are now so systemically important that letting them reprice would shake the financial system itself. The crash, people being forced into liquidation, was the one audit capitalism kept for itself, and it now comes with a standing promise that it won’t be allowed to finish.

3. Own the Inputs.

In one of the rural communities I’ve worked in, a family owns an aggregate mine outside town. Over a few generations the sequence went like this: control the local price of aggregates, win the state construction work that runs on aggregates, roll the profits into owning most of downtown including its operating businesses, become the bank’s favorite borrower (at some point the bank basically stopped pricing doubt, because doubting this family meant doubting the town), then use the credit to buy more productive assets.

They don’t have as much money as God. What they have is economic power: their demand sets local prices, and what they choose to fund sets local priorities. Nobody in this story is a villain and nobody broke a law, you don’t need a billionaire to collapse a local financial market into you. You need a structure where cash flows to you regardless of contribution and nothing can ever force you to sell. Sole ownership of basic inputs, whether that’s oil or aggregates or permitted land or water, does exactly that. Competitive markets in raw materials aren’t an economic nicety; instead they are essential democratic infrastructure. Whoever owns the only mine set the prices and economic direction through what they choose to consume and fund.

The Collapse

So, what do we call this thing? Everyone keeps reaching for “bubble,” but bubble is the wrong word. It stopped being a bubble sometime in the last 15 years when QE was used to fix wobbles.

A bubble is over-extended trust, optimism priced past what the assets underneath can honor, and it resolves the honest way: it pops, prices reset, the audit resumes. A popping bubble is the system’s fever breaking, but there’s a version of this the fever can’t fix.

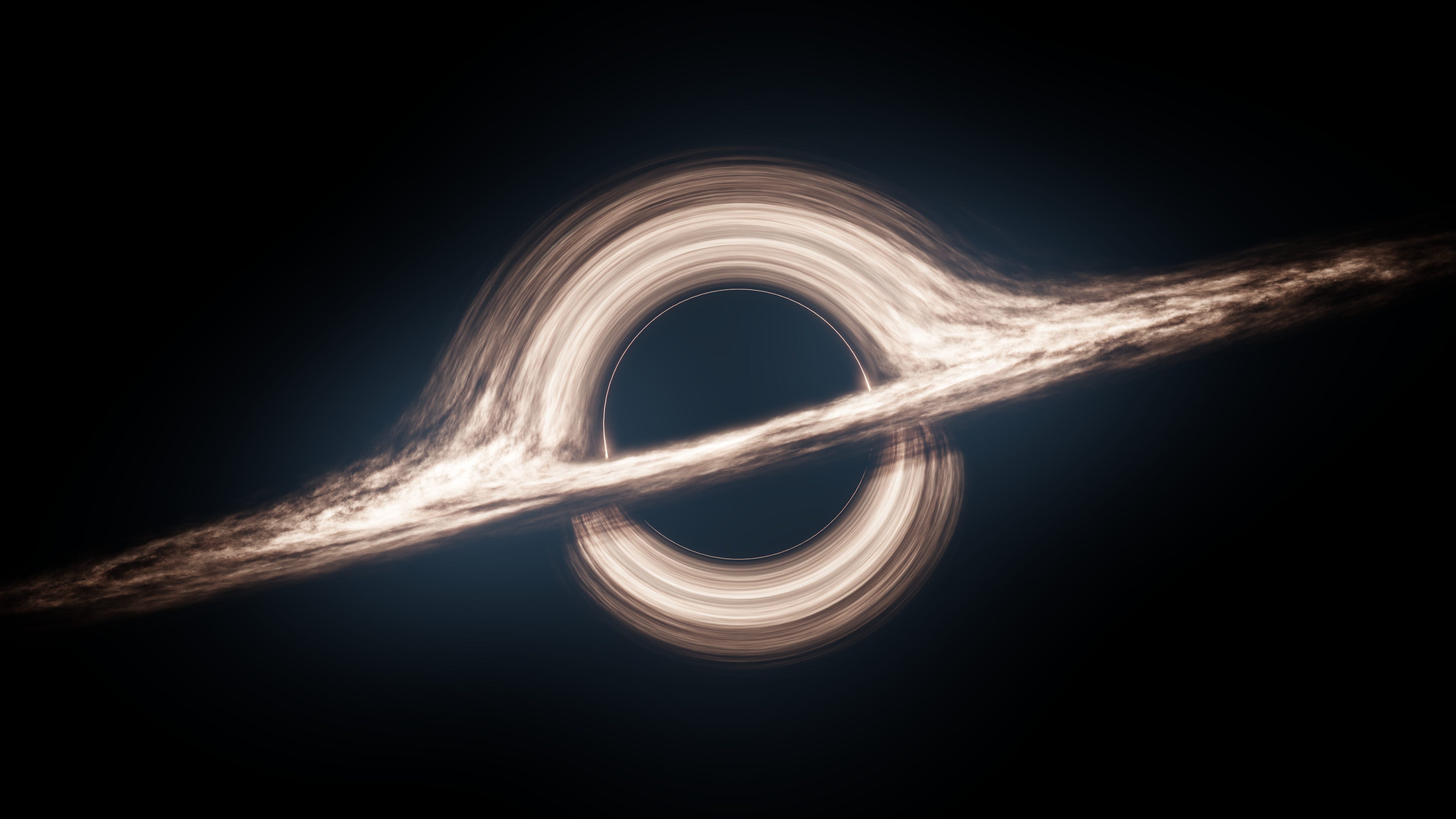

When a large star dies it explodes, however past a certain mass, the explosion loses to gravity and the core collapses inward into an object with an event horizon, a boundary past which nothing comes back out, not even light. Physics doesn’t end at the horizon, but it does change and the rules that govern everything else stop applying.

That’s what has happened here. A bubble got too big and too structural to be allowed to pop: index-fed, bailout-guaranteed, collateral to the banking system itself. And a bubble that isn’t permitted to pop does the only other thing it can do: it collapses into permanence. Too big to fail was the critical mass.

Earlier I gave the escape altitude a definition, the point where your assets appreciate faster than your interest plus your cost of living. Now I can call it what it is. It’s an event horizon, and it only opens one way. On this side of it the old physics hold: doubt has a price, sales get forced, taxes come due. Past it they don’t. Interest collapses toward zero because doubt has become impossible, the bank can’t doubt the family without doubting the town, and the Fed can’t doubt the collateral pools without doubting the system built on top of them. No sale is ever forced, so no price is ever discovered. Like light, the information doesn’t come back out. No gain is ever realized, so the public audit never arrives, and death doesn’t repatriate anyone because the basis steps up and the loan repays itself.

And the interior of this Economic Black Hole is a vacuum of trust. A vacuum is the absence of pressure, and the pressure that governs everyone else in the economy is the audit: the forced sale, the tax that comes due, the return that grades your judgment. Inside the horizon none of it reaches. Trust just piles up in there, unaudited, forever.

One more piece of astrophysics while we’re here. The brightest objects in the universe aren’t stars. They’re accretion disks, the glow of matter spiraling into a black hole, radiating on the way in. I called the index an intake fan earlier and this is the better name. The next time someone shows you a chart of all-time highs, ask yourself what’s making the light.

Wealth used to be a lagging indicator of problems solved. Inside the vacuum it’s a leading indicator of nothing but itself. That’s the weird feeling. Your gut isn’t confused and it isn’t envious. It has correctly noticed that part of the scoreboard slipped past the horizon and stopped counting.

Orbit

You can’t pop a vacuum and you can’t un-collapse a black hole. There’s no pin. The standing bailout intercepts every crash, and no election repeals compounding. I won’t pretend otherwise, because pretending is how you get hype, and hype is the accretion disk’s house style.

But gravity gives you two positions. You can spiral in, with your wages, rent, deposits, and index flows all drifting across the horizon, your output feeding a mass you’ll never get to audit. Or you can hold an orbit: enough owned mass, moving at enough velocity, to circle without falling - floating independently. In economic terms the mass is the assets that solve your own problems (the roof over your head, the tools of your trade, the firm that feeds you) and the velocity is cashflow that beats what gravity extracts from you in rent, interest, and fees. An orbit isn’t passive. Most average people never stop countering gravity, they just stop losing to it. There’s a whole playbook of orbital mechanics for operators in my next essay.

An orbit isn’t passive, and it isn’t reserved for the rich. The people holding one are mostly ordinary. They never stopped countering gravity, they just stopped losing to it.

And further out there’s a longer project: an economy where inputs stay contested, where credit still carries doubt, where trust has to keep passing all three audits to keep its name.

Somewhere tonight there’s a seventeen-year-old closing a kitchen next to a forty-year-old doing the same job, both passing the audit that never ends, both feeding, through rent and deposits and the index, a mass on the far side of a horizon where the audit never begins.

Close

Everyone is still waiting for the bubble to pop. But unfortunately it may have collapsed. Black holes don’t pop; they pull. You don’t get a vote on the gravity. You get a vote on your trajectory.

If you’re a founder or operator building your orbit — turning cashflow into owned mass — I would like to talk. If you’re a capital allocator trying to figure out what returns mean once price stops being a verdict, happy to discuss. And if you’re still on the line, passing the audit in your business every two weeks and wondering whether orbit is even reachable from where you stand, that is the conversation I most want to have. duncan@saorsapartners.com

Subscribe to Conduit of Value for the next piece: the orbital mechanics playbook — which assets count as mass, how much velocity is enough, and how close you can safely orbit something that big. This piece is a companion to Jobs Are Dead, which argued the market now pays a premium for builders. This one names the gravity every builder is building against.

One question to leave you with, and I read every reply:

What’s the one asset that would flip your trajectory from spiral to orbit and what’s actually standing between you and it?